Mortgage Rates Today: What's Driving Them and The Opportunities Unfolding

The Great Mortgage Rate Reawakening: Why This Moment Demands Your Intelligent Action

Alright, let's talk about something truly exciting, something that’s quietly, powerfully shifting the ground beneath our feet, and frankly, I don't think enough people are grasping the full scope of it yet. We’re not just seeing numbers tick down; we’re witnessing a genuine reawakening in the mortgage market, a potential paradigm shift for homeowners and aspiring buyers alike. And honestly, when I first saw the latest data, I just had to sit back and let it sink in—this is the kind of breakthrough that reminds me why I got into this field in the first place, seeing how big data can illuminate human opportunity.

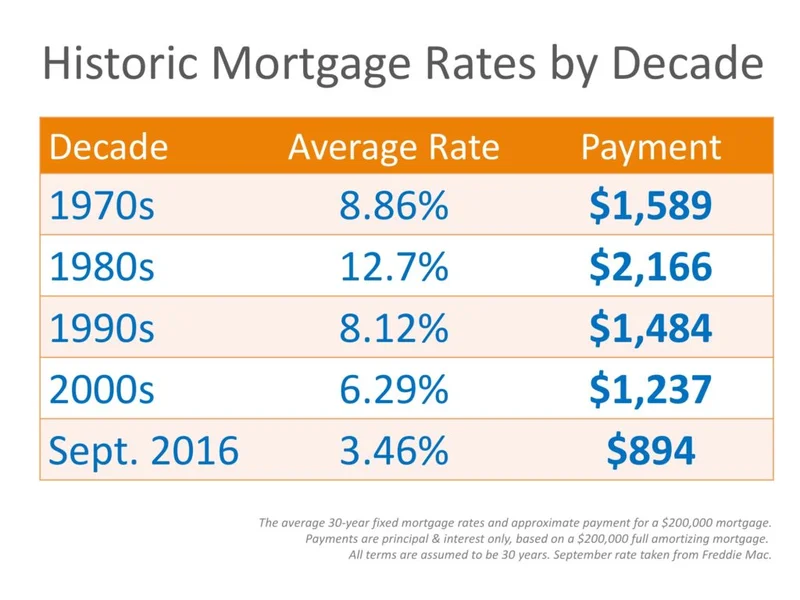

For what feels like an eternity, the American Dream of homeownership, or even just the sensible act of refinancing, has felt like pushing a boulder uphill. Mortgage interest rates, those silent, relentless gravitational pulls on our finances, have been stubbornly high, often hovering north of 7%. It’s been tough, disheartening even, for so many. But here’s the kicker: as of late November 2025, those rates are doing something truly remarkable. We've seen the average 30-year fixed-rate mortgage dip to 6.03% APR on one day, then even touch 5.99% APR on another. And the 15-year fixed-rate? Down to 5.46% APR. Now, I know what some of you might be thinking, "Aris, it's just a few basis points," and yes, a basis point is just a hundredth of a percent, or 0.01%, but trust me, these aren't just minor fluctuations; they're whispers of a much larger narrative unfolding.

The Shifting Tides: What the Numbers Really Tell Us

This isn't just some random market wobble; there’s a distinct, intelligent force behind these shifts. The buzz from the financial community, the quiet hum that’s starting to grow louder, is all about the Federal Reserve. The market has become increasingly convinced—and frankly, I agree with this assessment—that the Fed is gearing up to cut short-term interest rates in December. Why? Because the signals from the labor market, particularly those recent ADP job loss figures, are pointing towards a softening economy. It’s like the market is a giant, anticipatory organism, already pricing in what it believes the Fed will do. We're seeing prominent figures like New York Fed president John Williams and others hinting at their support for cuts, which, for anyone paying attention, is a pretty strong indicator. According to Mortgage rates dropped this week amid fresh signs of job market weakness, job market weakness is a key factor.

Think of it like this: for years, we’ve been sailing against a strong headwind, but now, the wind is starting to shift, potentially even at our backs. This isn't just about saving a few bucks next month; it’s about the cumulative impact over the life of a loan, the kind of monumental financial breathing room that can redefine a family's budget for decades. That 30-year fixed rate, now a full 51 basis points lower than a year ago, is a significant marker. It’s not just a drop; it’s a sustained downward trend that’s bringing rates near their 2025-lows just as the year closes out, and that's huge, absolutely huge, for anyone who's been waiting on the sidelines. What does this truly mean for the fabric of our communities, for the young families eager to put down roots, or for those looking to tap into their hard-earned home equity? It means opportunity, plain and simple.

Beyond the Horizon: Seizing Your Financial Future

This moment, my friends, is a powerful call to action for the intelligent homeowner. For hundreds of thousands of you who locked in rates around 7% or higher in the tougher times of recent years, this is your refinance opportunity. Seriously, we’re talking about potentially shaving thousands, even tens of thousands, off the total cost of your loan. Imagine what that extra capital, that freed-up monthly cash flow, could do for your family – investments, education, even just a deeper sense of security. It’s not just theory; the data from Freddie Mac shows that comparing even just a few lenders can save you up to $1,200 annually, and over the life of a loan, a mere quarter-percentage point difference can translate to almost $22,000 in savings. That’s real money, enough to fund a child’s first car or a significant chunk of a college fund.

This isn't just a fleeting moment; it's a potential turning point, echoing historical shifts where shrewd individuals made moves that paid dividends for generations. Just as the advent of personal computing democratized information, these shifting mortgage rates are democratizing financial agency. We’re moving into an era where being proactive, understanding the macro forces at play – like the global economy, the Fed’s decisions, and even our own credit scores and down payments – can empower us in ways that seemed impossible just months ago. But here's a crucial ethical consideration: with great opportunity comes great responsibility. This isn't an invitation for reckless borrowing, but for informed, strategic action. Understand your budget, evaluate your long-term goals, and make choices that truly align with your vision for the future. Don't just chase the lowest number; chase the smartest number for you.

The housing market is already responding, showing light tailwinds with contract signings up and purchase applications on the rise. Some might dismiss these as minor bumps, but I see the quiet confidence of buyers returning, the hopeful glint in the eye of a homeowner realizing they might finally be able to shed that higher rate. This isn't just good news for individual pocketbooks; it's a positive ripple effect throughout the entire economy, breathing new life into local communities.

The Dawn of Financial Empowerment

So, what does this all boil down to? It’s simple: the financial landscape is changing, and the smart money is moving. We’re at the cusp of what could be a sustained period of more favorable borrowing conditions, a window of opportunity that’s been stubbornly shut for too long. This isn't the time for complacency; it's the time for intelligent action. Whether you're eyeing that first home, looking to secure a better refinance rate, or simply want to understand how these seismic shifts impact your personal financial universe, the data is clear: the future is calling, and it’s inviting you to take control.